Macroeconomic headwinds trouble global markets

Investor sentiment remains gloomy. Ongoing supply chain disruptions, new lockdowns in China, and war-related food and fuel shortages are weighing on businesses and investors.

These issues have aggravated worries that persistently higher inflation and the Fed’s effort to contain it will trigger a recession or even stagflation.

The U.S. 10-year Treasury yield almost doubled from 1.6% at the end of 2021 to around 3% by May 2022. Equity markets have sold off alongside rates and credit.

The MSCI All Country World Index, a measure of global equity performance, was down 12.8% year-to-date as of May 31, 2022.

So far this year, only a handful of industries have delivered positive results — chiefly energy, mining and tobacco producers. They are heavily represented in value indices, which helps explain value’s recent outperformance.

Conversely, companies with growth profiles have been the hardest hit. Traditional growth sectors, including consumer discretionary, media and information technology, have led the underperformers.

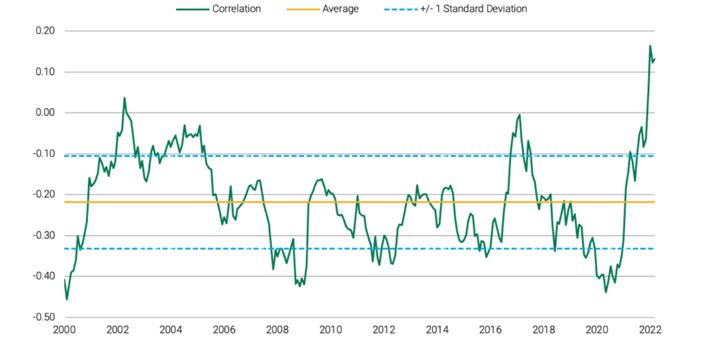

Correlation of momentum and value factors at 20-year highs

While the rotation into the more defensive categories may continue, we see indications the shift away from growth may be peaking.

The figure below shows how the correlation of value and dividend yield factors to momentum is at levels not seen since the technology crash in 2001.

Meanwhile, the correlation of growth factors to momentum has headed in the opposite direction.

Correlation of value and momentum factors

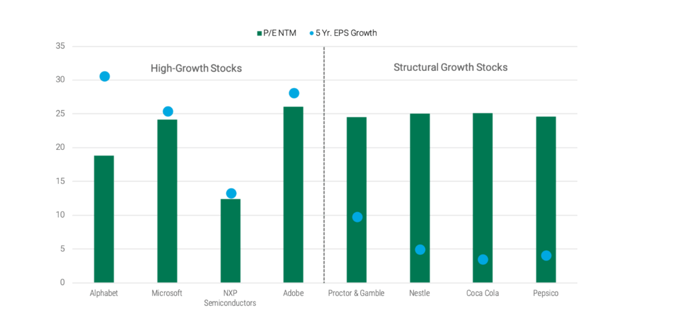

Select defensive stocks are priced like fast growers

The strong outperformance of perceived defensive businesses in the food and household goods categories has resulted in a rerating of those stocks.

In some instances, low structural growers are trading at multiples comparable to faster-growing companies.

Some unloved growth stocks are trading at similar multiples with slow structural drivers

Inflationary pressure may be peaking

Higher inflation and rising interest rates tend to be less of a headwind for value stocks. We expect economic growth to slow and inflationary pressures to stabilize.

We think this will put a premium on companies that can sustain their earnings growth in this environment and create a more favourable backdrop for growth stocks.

Still, the timing of when inflationary pressures might ease remains highly uncertain.

The prices of copper and other commodities have already fallen from recent peaks, but pricing remains elevated in areas like travel (e.g., airlines, car rentals) and the labour market.

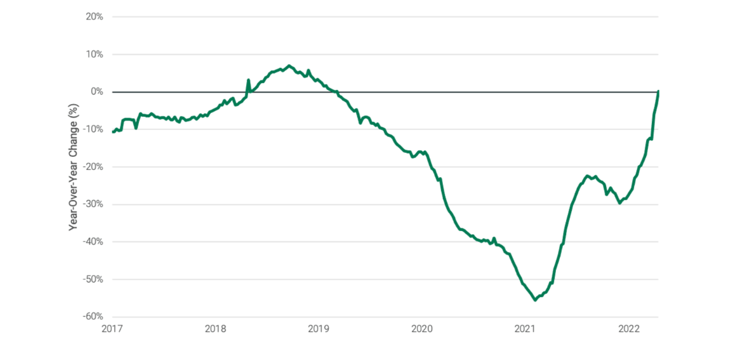

Housing market may be poised to cool

Housing is the largest component of the Personal Consumption Expenditures Price Index and Consumer Price Index.

It’s also been one of the hottest segments of the U.S. economy due to attractive mortgage rates and tight inventory.

However, we think there are indications these tailwinds may be starting to lessen. For example, mortgage rates have begun to rise, and we’ve seen evidence that tight housing inventories may be loosening.

In absolute terms, the number of available houses remains low compared to historical trends.

The figure below shows that the growth of active listings on a year-over-year basis has turned up compared to nearly three years of decline. The rise in listings indicates the supply of houses is growing.

Weekly active home listings increase

Stick with your long-term plans

As higher rates begin to pressure demand and take inflation lower, we would expect growth’s underperformance to plateau.

However, we caution that timing factor performance and forecasting inflation are extremely difficult. In periods of market volatility, it is important not to overreact and stick with long-term investment strategies.

Ted Harlan is a portfolio manager for American Century Investments.