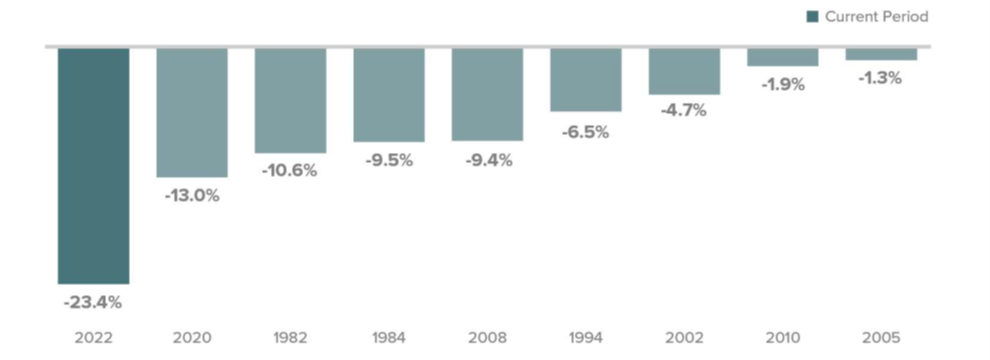

The small-cap Russel 2000 index fell 23.4% for the year-to-date period ending 6/30/22 – which was the worst first-half performance in its more than 40-year history by a significant amount.

Francis Gannon, co-chief investment officer and managing director of Royce Investment Partners, said: “While the historic depth of the decline was surprising, a negative result for small-cap stocks was not.

“A highly inhospitable climate consisting of restrictive Fed policies, increasing fears of recession, and persistent inflation combined to create the conditions for lower returns for most small-cap stocks.”

Small-cap’s dubious achievement

Negative calendar year first-half returns for the Russell 2000 index since 1978 inception

The second quarter of 2022 offered no safe haven for investors as these same factors, along with higher energy prices, conspired to drive prices lower – regardless of asset class, style or geography.

The small-cap Russell 2000 index lost 17.2% in the second quarter, slightly lagging behind the large-cap Russell 1000 index, which fell 16.7% for the same period.

Historically, the second quarter of this year ranked eleventh worst out of the 59 down quarters for the Russell 2000 since its 1978 inception.

“The most notable performance spreads were not rooted in capitalization but in style, as growth stocks suffered more than their value siblings across asset classes,” said Gannon.

“With interest rates rising sharply, these relative results were consistent with our view that growth stocks face considerable duration exposure, arguably more than investors appreciate.”

The Russell 2000 Value index was down 15.3%, outperforming the Russell 2000 Growth index – which fell 19.3% – and recording small-cap value’s seventh consecutive quarter of outperformance.

In the shadow of the small-cap bear

Gannon highlighted that while the major US equity indices sustained comparable losses for the quarter, Q2 extended a longer bearish pattern for small-cap stocks.

The Russell 2000 lost nearly 32% from its peak in November 2021 through the small-cap low on 6 June 2022.

“As is the case during small-cap down markets, the degree to which the index fell understates the depth to which the average small-cap stock declined – a loss of 48% for the average stock in the index from their respective 52-week highs through the mid-June low.

“We think it’s important to note that the current depth of the of the small-cap market’s swoon is comparable to the median drawdown for the twelve declines of 20% or more since the Russell 2000’s inception.

Gannon highlighted that while the major US equity indexes sustained comparable losses for the quarter, Q2 extended a longer bearish pattern for small-cap stocks.

The Russell 2000 lost nearly 32% from its peak in November 2021 through the small-cap low on 6 June 2022.

“As is the case during small-cap down markets, the degree to which the index fell understates the depth to which the average small-cap stock declined – a loss of 48% for the average stock in the index from their respective 52-week highs through the mid-June low.

“We think it’s important to note that the current depth of the of the small-cap market’s swoon is comparable to the median drawdown for the twelve declines of 20% or more since the Russell 2000’s inception.

“History suggests that the bulk of the small-cap decline is likely behind us,” he argued.

The case for small-cap

Challenging markets traditionally offer investors a good opportunity to enter the market.

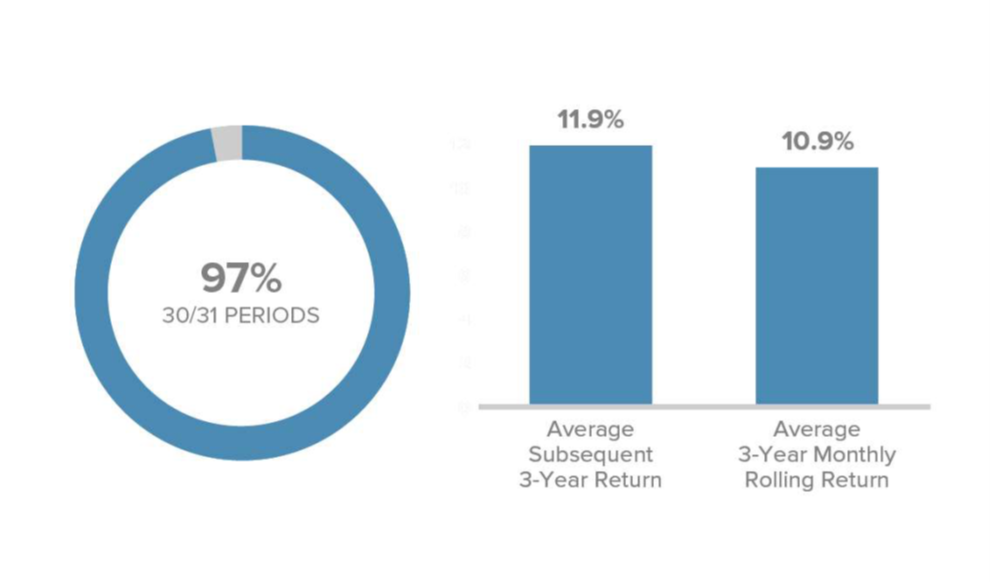

Gannon pointed to research from the Center for Research in Security Prices at the University of Chicago which dates to 1945 and shows that small-cap stocks have posted positive annualized three-year returns 88% of the time on a rolling monthly basis, with an average return in the low double digits.

“To this degree, history offers clarity amid the uncertainty,” he said.

“Equally, if not more important, we have found the most opportune times to invest are when fear is high and trailing returns are low.”

The VIX (CBOE Volatility Index) is currently flashing a fear signal ending June in the top 20% of the highest average monthly readings since its inception.

“Subsequent returns from these levels have been attractive – for investors with the fortitude to act,” Gannon added.

Subsequent average annualized 3-year performance for the Russell 2000 following 3-year annualized return ranges of 0-5%

The annualized three-year return for the Russell 2000 at the end of June was 4.2% compared to its three-year monthly rolling average since inception of 10.9%.

Subsequent annualized three-year returns for small-cap from comparable trailing low return entry points have been positive 97% of the time since the Russell 2000’s inception – averaging 11.9%.