‘Greenflation’ refers to the sharp rise in the price of materials and minerals used in the creation of green technologies.

As higher costs are expected to feed into consumer prices, greenflation more generally defines high consumer inflation that relates to the transition to net zero.

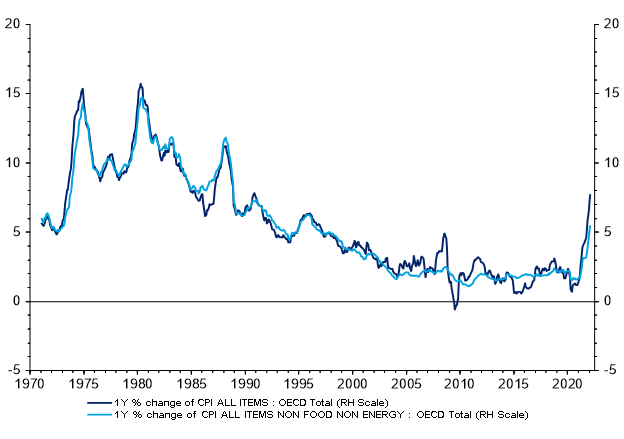

Consumer price inflation has increased sharply across the board over the last year, fueling the hype surrounding greenflation.

Organization for Economic Co-operation and Development (OECD) inflation increased to 7.7% in February 2022 – a record high since November 1990 – up sharply from a pandemic trough of 0.7% in May 2020.

The easiest way to assess current greenflation is to focus on energy inflation.

Energy accounts for a small share of the Consumer Price Index (CPI) basket – varying between 5% and 16% across OECD countries in 2020.

Yet it is typically responsible for large contributions to headline inflation, due to its pronounced volatility.

That has continued to hold during the lower and less-volatile inflation regime that has prevailed since the mid-90s.

Over this period OECD energy CPI inflation has swung between -18% year-on-year and +28% year-on-year, standing out as the main driver of volatility in headline inflation.

Ripple effect of higher energy prices

Changes in energy prices are typically short-lived and mean-reverting but can affect other sectors and cause a more pervasive, long-lasting impact on overall inflation.

Since the mid-90s, oil inflation has displayed a correlation with OECD food inflation, unsurprising given energy is a significant input for the sector.

By contrast, over the same period, the correlation between oil inflation and OECD core CPI inflation, excluding energy and food, has been negligible. This may reflect the overwhelming impact on inflation from other factors, such as globalization and automation.

Temporary evolutions in energy prices can affect overall inflation through other channels.

Low or high inflation due to energy prices can become embedded via second-round effects. In other words, if and to the extent it affects long-term inflation expectations and/or wage dynamics.

Additionally, while an increase in energy prices immediately results in high inflation, it is also an income shock that can eventually result in lower inflation. Cost-push inflation is generally self-defeating, as it results in real income erosion and weaker aggregate demand.

In the last decade, the narrative on greenflation has tended to shift depending on whether oil prices have gone up or down.

In 2014-16, Brent crude oil prices fell sharply by about 76% peak-to-trough. The single most important driver came from the supply side: Saudi Arabia deliberately increased its supply to squeeze US shale competitors facing higher production costs.

Other factors were mentioned, including weaker Chinese demand and competition from renewable energy sources.

So, the prevailing narrative was that the net-zero transition was likely to create disinflationary pressures via its impact on energy costs.

Fast forward to 2021-2022, and energy commodity prices have been on a steep upward trend since around mid-2020 following the acute phase of the pandemic.

As of mid-March 2022, oil prices are up more than 50% compared to early 2020 levels. Accordingly, OECD energy CPI inflation came in at 27% in February 2022.

Energy inflation has made large contributions to headline inflation across the board: it accounted for almost 25% of headline inflation in the US and about 60% of headline inflation in the Eurozone in February 2022.

More to the story

The transition to net-zero is just one factor within a much more complex picture of factors driving inflation.

These include pandemic-related supply and demand distortions; a failure to invest enough in energy sources required as a buffer for the transition from fossil fuels to renewables; higher gas demand from China; and, crucially, geopolitical tensions – most recently the Russia-Ukraine conflict.

The transition to net-zero has probably contributed to the recent surge in energy inflation alongside other and probably more significant drivers.

In this complex context, where several interacting factors have converged, it is hard to quantify the exact contribution from greenflation to current inflation.

Going forward, fossil fuels are set to be replaced by cheaper and more efficient energy sources.

In the long-term, the transition to net-zero will deliver lower energy costs. These costs have already fallen by more than expected in a relatively short time, as investments in new and greener technologies have picked up in the last decade.

Silvia Dall ‘Angelo is a senior economist at Federated Hermes Limited